How much can you gift a person tax-free? Yes, but with caps and stipulations. From a tax perspective, promotional products tax deductions under IRS rules are typically deductible as ordinary business expenses, allowing subtraction from gross income to compute taxable amounts—provided they align with IRS Publication 535: Business Expenses guidelines. In corporate promotional gifts procurement, deductibility profoundly sways decisions, molding budgets and ROI for branded swag campaigns. If fully or partially excludable, firms gravitate toward ample, value-laden assets. Grasping qualifying swag fosters compliant filings, averting fiscal faux pas.

Yet, specifics hinge on national codes and utility/valuation. Below, a granular dissection:

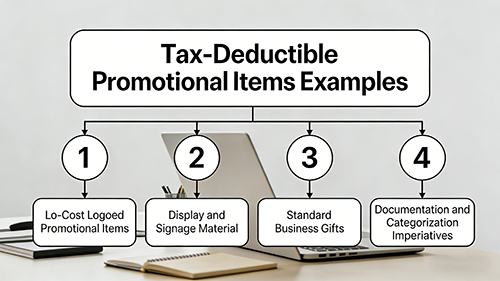

Tax-Deductible Promotional Items Examples: Qualifying Low-Cost and Advertising Assets

Broadly, marketing/branding tools qualify as ad/promotional outlays. Archetypes include:

(1) Low-Cost Logoed Promotional Items E.g., pens, calendars, mugs, plastic bags—imprinted with firm names/logos, capped at $4 per unit tax-free promotional products threshold for full exclusion as ads, bypassing the $25 gift cap per recipient annually. These aren't "business gifts," evading per-person limits.

(2) Display and Signage Materials Showcases (racks), banners, posters, or client-site collaterals—deemed ad/marketing per IRS Publication 463: Travel, Gift, and Car Expenses, fully deductible.

(3) Standard Business Gifts Modest office sundries like USBs, mouse pads, stands—capped at $25 annual business gift deduction limit per recipient, inclusive of indirects (spouses count singly). Exceptions: Low-cost promotional items under $4 with logos in mass distribution sidestep this, as do incidental packaging/shipping/engraving sans substantive value-adds. Meticulous logging is mandatory.

(4) Documentation and Categorization Imperatives Ledger as "promotion expense" vs. gifts—hoard invoices, dispersal logs (recipients, dates), descriptors for audits/filings, ensuring IRS-compliant promotional products record-keeping.

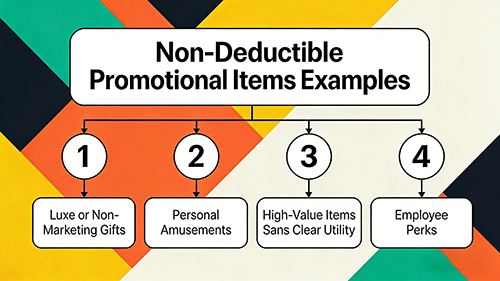

Non-Deductible Promotional Items Examples: Pitfalls to Avoid in Swag Tax Planning

Ambiguous utilities or excesses may bar exclusions:

(1) Luxe or Non-Marketing Gifts Elite tokens to staff/non-clients—hard to substantiate as ads.

(2) Personal Amusements Irrelevant to revenue/reach.

(3) High-Value Items Sans Clear Utility Breaching caps or undocumented—ineligible.

(4) Employee Perks Wage/benefit routes, not ads.

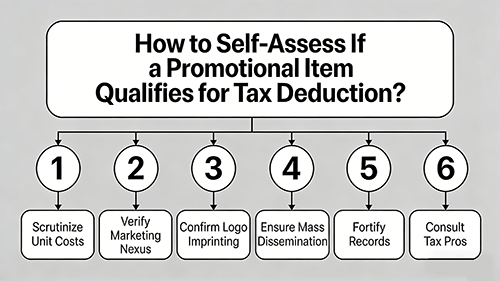

How to Self-Assess If a Promotional Item Qualifies for Tax Deduction: Practical IRS Checklist

(1) Scrutinize Unit Costs Verify inclusions (imprinting/customs)—low-cost promotional items ≤$4 snag special ad treatment; premiums trigger $25/person/year caps, with overruns nondeductible—yet boundless spending persists.

(2) Verify Marketing Nexus Ad/branding/client nurturing/conference ties?

(3) Confirm Logo Imprinting Permanent (screening, foiling) on prospect/client dispersals—bolstering ad claims.

(4) Ensure Mass Dissemination Broad casts (meets, expos, client conclaves) underscore marketing vs. singular "gifts."

(5) Fortify Records Invoices, ledgers (recipients, firms, quanta), uses—proving tax deduction documentation for promotional swag.

(6) Consult Tax Pros Rules vary by entity (C-corps, LLCs, S-corps), accounting (cash/accrual)—pre-major outlays, query CPAs.

Assessing promotional items tax deductibility IRS 2025 pivots on utility, valuation, marking, and manifests. As ad/marketing conduits with judicious costs and chronicles, they qualify fully—easing burdens while honing promotional budgeting strategies, magnifying yields sans lapses.